Video Game Industry Revenue in 2026: 3.6 Billion Players and a $188 Billion Market

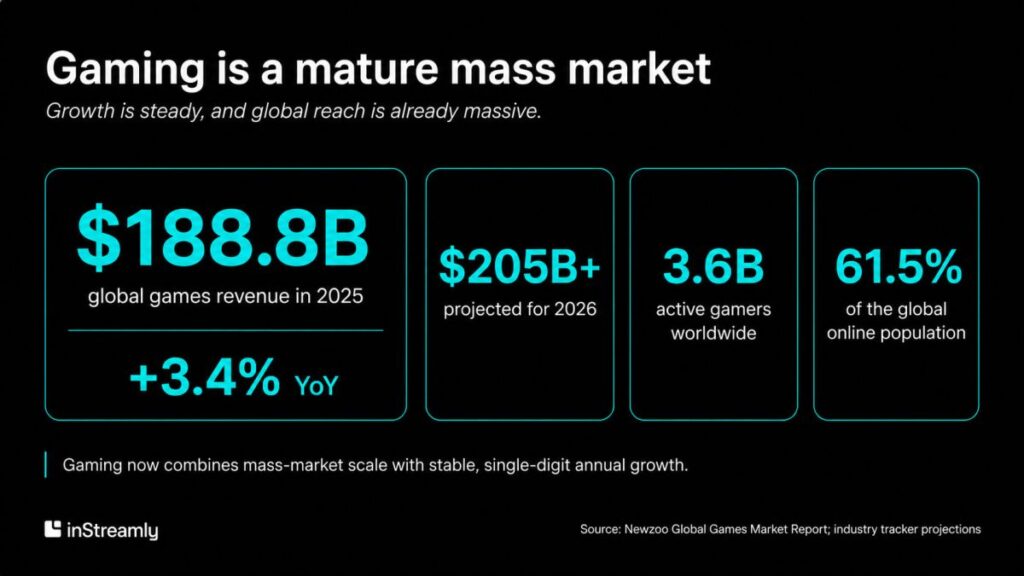

The global video game industry generated $188.8 billion in revenue in 2025, and it is on track to reach roughly $205 billion in 2026. That single figure is larger than the global box office and recorded music industries put together. Behind it sits an audience of 3.6 billion players, more than 61% of everyone online.

Most media plans still file gaming under “specialist channel.” That filing is a measurement error. A market this large, growing this steadily, with this much of the under-35 population inside it, is not a niche. It is the largest entertainment category on the planet by both money and reach.

This article lays out the revenue, the platform split, and the audience numbers. Then it covers the part that matters for a media buyer: what the size of the gaming market actually changes about how you plan to reach people.

How much revenue does the video game industry generate?

The video game industry generated $188.8 billion in revenue in 2025, up 3.4% year over year, according to Newzoo’s Global Games Market Report. Industry trackers project global video game industry revenue to pass $205 billion in 2026. Growth is no longer the explosive expansion of the pandemic years. It is steady, single-to-mid single digit annual growth, which is the profile of a mature mass market rather than a passing trend.

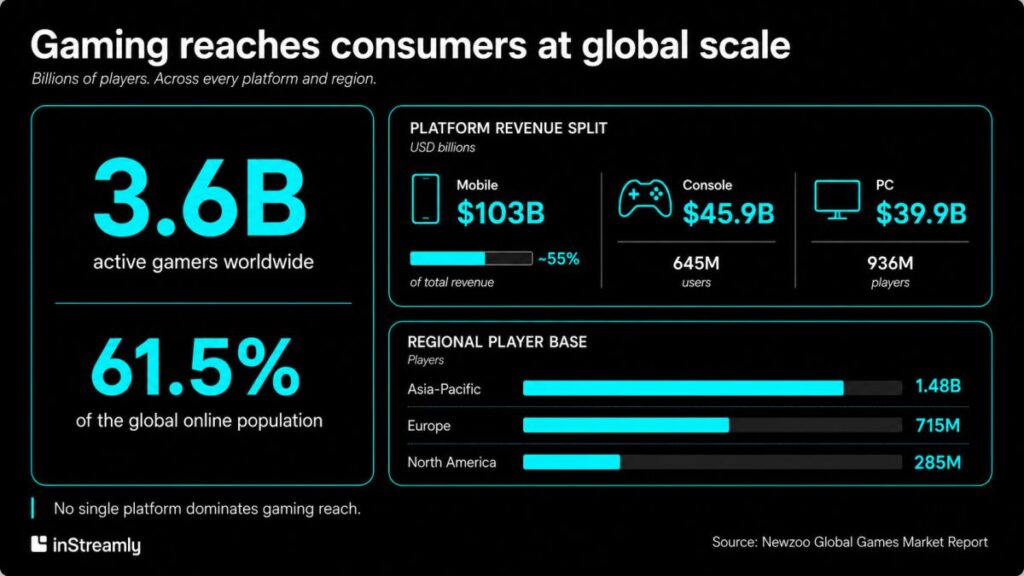

The player count tells the reach story. There are 3.6 billion active gamers worldwide, which Newzoo puts at 61.5% of the global online population. That is a larger share of internet users than any single social platform reaches.

The revenue splits across three platforms:

- Mobile: $103 billion, about 55% of the total

- Console: $45.9 billion across 645 million users

- PC: $39.9 billion across 936 million players

No single platform dominates the audience, which means a brand cannot reach gamers through one device or one storefront.

The audience is also global, not concentrated in a few mature markets:

- Asia-Pacific: roughly 1.48 billion players

- Europe: near 715 million

- North America: near 285 million

The United States and China together drive about half of total revenue, but the player base sits everywhere. For a brand planning across regions, that spread is the point. Gaming reaches the same consumers a brand is already trying to find through other channels, in almost every market that matters.

Video game industry revenue by year

Video game industry revenue has held in the $180 billion range since 2022 and is climbing again. The trajectory:

- 2022 to 2024: a slight post-pandemic dip, then a plateau in the low-to-mid $180 billions

- 2025: $188.8 billion, up 3.4% year over year

- 2026 (projected): roughly $205 billion

One caveat matters when you compare years. Newzoo periodically restates its historical figures as methodology changes, so a headline growth rate always refers to a revised baseline rather than the number printed in an earlier report. For a like-for-like year-over-year view, use a single report edition rather than stitching figures across reports.

Who actually plays games in 2026?

A far broader group than the stereotype suggests. Women are close to half of all players globally, the average gamer is 41, and gaming now spans every generation. The teenage-boy gamer is a real but shrinking minority of the audience, and the data has moved a long way from it.

The ESA’s 2025 Global Power of Play study surveyed 24,216 active gamers across 21 countries. The headline numbers:

- Gender: 48% of gamers globally are women and 51% are men. In the United States, women are the majority at 52%.

- Markets where women lead: female gamers outnumber men in several national markets, including Brazil and South Africa.

- Age: the average gamer is 41 years old, and players aged 50 and over now make up about 30% of the total base.

For the deeper breakdown on this audience, inStreamly has a full analysis of female gamers in 2026.

The planning implication is direct. “Gaming audience” is no longer a sub-segment you target around the edges of a campaign. It is close to a one-to-one match for “mainstream consumer audience.” If you want a closer look at the full picture, inStreamly’s 2026 gamer demographics breakdown covers age, gender, and device in detail.

Mobile, console, and PC each reach a different audience

The platform split is not just a revenue chart. Each platform serves a different audience with different behavior, and that matters when you decide where a campaign lives:

- Mobile holds 55% of revenue and the broadest, most geographically spread audience. It is the entry point for players in growth regions and the platform where casual and core players overlap most.

- Console commands deeper, longer engagement sessions and a more committed core audience, anchored by predictable release cycles and flagship titles.

- PC sits at 936 million players, the largest player base of the three hardware platforms, concentrated around storefronts and live-service titles.

One structural trend cuts across all three: the model is shifting from ownership toward access. Subscription services and cloud gaming are pulling players away from buying individual titles and toward paying for libraries and on-demand streaming. For a media buyer, the takeaway is less about which platform wins and more about the fact that gaming attention is fragmented across devices and access models at once. Reaching it requires a delivery method that works across that fragmentation rather than betting on one screen.

Live streaming turns the gaming audience into a reachable one

A large audience is only useful to a brand if there is a place to reach it. For gaming, that place is live streaming, and the scale is now substantial:

- 36.4 billion hours of gaming live content watched globally in 2025, up 6% year over year, according to Stream Hatchet

- Twitch alone: 19.2 billion hours watched across the year, still the most-watched platform

This is not a fringe behavior. It is hundreds of millions of people spending hours per week watching other people play.

What makes this audience reachable is how they treat advertising inside the stream. According to inStreamly’s Live Streaming Trends 2025 report, 79% of Twitch viewers see in-stream brand integrations as a way to support their favorite creators rather than as interruptions. That is the opposite of how the same audience treats display advertising, which most of them block.

The attention this format earns also behaves differently:

- Standard display ads: a couple of seconds of attention at best

- Contextual gaming activations: minutes at a time, inside content the viewer chose to watch for hours

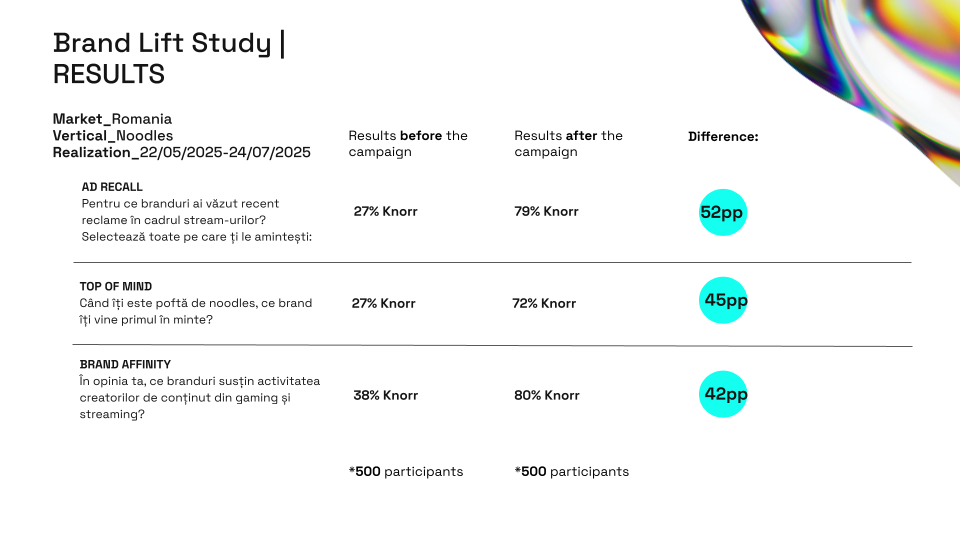

A brand is not buying a fraction of a second of skippable exposure. It is appearing inside the thing the viewer came for. That gap is measurable. inStreamly’s Knorr campaign in Romania, for example, recorded a 52 percentage point lift in ad recall for a non-endemic brand by timing branded moments to the stream rather than buying interruptive placements.

Why does traditional media miss most of this audience?

Two structural reasons: most of this audience blocks ads, and most of it has left traditional TV. Both are measurable, and together they explain why a large, valuable audience stays invisible to conventional buys:

- Ad blocking: 64% of stream viewers use ad-blocking tools, and over 900 million people use ad blockers worldwide. Platform crackdowns have not reversed the behavior, so standard display does not reach the majority of this audience.

- TV abandonment: 62% of livestream viewers have abandoned traditional TV entirely, with a quarter saying they do not even have access to it.

One more figure belongs next to these, and it is a separate fact, not the same one: 73% of stream viewers are aged 16 to 34. The under-35 audience is both the most valuable to many brands and the least reachable through the channels media plans default to. A TV buy and a display buy together will miss a large part of the people a brand most wants.

This is the structural case for gaming as a channel. The audience is enormous, engaged, and largely invisible to legacy media. The format that reaches them has to be built for the environment they actually spend time in.

What the gaming market’s size means for your media plan

The data points in one direction. A brand that treats gaming as optional is choosing to skip more than 60% of internet users, and a disproportionate share of the under-35 consumers inside that group.

For audiences under 35, gaming and live streaming are not an add-on reach channel. For many of them they are the primary one, ahead of the television and display formats that still take the largest line items in most plans. The mismatch between where the audience is and where the budget goes is the planning gap worth closing.

Two practical moves follow from the data:

- Give gaming its own budget line, measured on its own terms, rather than treating it as a reallocation from influencer marketing.

- Hold it to real metrics. Contextual live streaming campaigns now report brand lift, recall, and verified human engagement the same way a media buyer expects from any serious channel. The Knorr result above is one example of brand lift measured against a control.

The question is no longer whether gaming reach can be measured. It is whether a plan can keep justifying the absence of a channel that reaches the audience this well.

Key takeaways

- The gaming market is mass, not niche. At $188.8 billion in 2025 and 3.6 billion players, it is larger than global box office and recorded music combined and reaches over 61% of internet users.

- The audience is mainstream. Women are 48% of gamers globally and a majority in the US, the average gamer is 41, and players over 50 make up roughly 30% of the base.

- Legacy media misses them. 64% of stream viewers use ad blockers and 62% have abandoned traditional TV, while live streaming drew 36.4 billion hours of gaming content in 2025. Gaming deserves its own budget line, not a reallocation.